Clogged Metropolitan Arteries

Bad conditions of mobility and accessibility to jobs and services in most metropolitan regions in developing countries are a key development issue. Besides the negative effects on the wellbeing…

Bad conditions of mobility and accessibility to jobs and services in most metropolitan regions in developing countries are a key development issue. Besides the negative effects on the wellbeing…

The 2014 baseline for the global economy still appears to be trending upwards, but the Year of the Horse may be jumpy.

Book launch (2014-01-29) - "Dealing with the challenges of macro financial linkages in emerging markets" Click here to download To watch the book launch, click here or copy and paste…

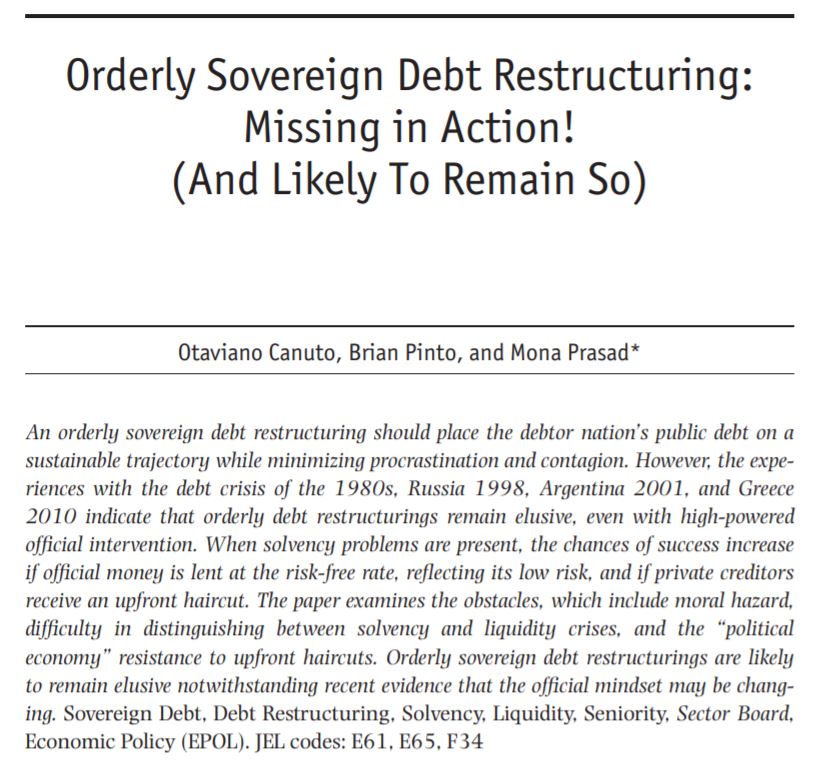

An orderly sovereign debt restructuring should place the debtor nation's public debt on a sustainable trajectory while minimizing procrastination and contagion. However, the experiences with the debt crisis of…

An orderly sovereign debt restructuring should place the debtor nation's public debt on a sustainable trajectory while minimizing procrastination and contagion. However, the experiences with the debt crisis of the 1980s, Russia 1998, Argentina 2001, and Greece 2010 indicate that orderly debt restructurings remain elusive, even with high-powered official intervention. When solvency problems are present, the chances of success increase if official money is lent at the risk-free rate, reflecting its low risk, and if private creditors receive an upfront haircut. The paper examines the obstacles, which include moral hazard, difficulty in distinguishing between solvency and liquidity crises, and the “political economy” resistance to upfront haircuts. Orderly sovereign debt restructurings are likely to remain elusive notwithstanding recent evidence that the official mindset may be changing.

Otaviano Canuto fala como o Brasil pode sair da "armadilha da renda média" Ex-vice-presidente do Banco Mundial explica também se priorização de investimentos em logística no País realmente valem…

The global economy looks poised to display better growth performance in 2014. Leading indicators are pointing upward – or at least to stability – in major growth poles. However, for this to translate into reality policymakers will need to be nimble enough to calibrate responses to idiosyncratic challenges.

Global financial integration and the linkages between the financial and the real sides of economies are sources of huge policy challenges. This is now beyond doubt, after what we saw in the run-up to and the unfolding of the 2008 global financial crisis. As a consequence, the established wisdom regarding monetary policies and prudential regulation has been subject to a deep critical review, including a demise of the belief that they should be maintained as fully independent functions.

Para onde vai a economia brasileira, segundo Otaviano Canuto Assessor-sênior do Banco Mundial explica a lógica por trás do ciclo virtuoso do país e como podemos caminhar para um…

https://soundcloud.com/riobravoinvestimentos/otaviano-canuto-complacencia-nas-economias-emergentes?utm_source=soundcloud&utm_campaign=share&utm_medium=twitter Conversamos com Otaviano Canuto, o senior advisor do Banco Mundial para os BRICS, um cargo criado pelo atual presidente do banco para gerar mais pesquisas sobre as maiores…

Not long ago, many economists were anticipating a switchover in the global economy's main engines, with autonomous sources of growth in developing economies compensating for the drag of struggling advanced economies. But, in the last few months, enthusiasm about these economies’ prospects has given way to bleak forecasts.

There are still serious questions on how to proceed with the complementary use of prudential regulation and monetary policy. While there are already lessons from emerging markets’ use of the macroprudential policy toolkit, more experience and analysis, particularly on its interaction with monetary policy is needed.

Emerging Markets (EMs) are more likely to suffer shocks, such as commodity-price and terms-of-trade shocks, as well as surges and sudden stops in capital flows.. Furthermore, structural and institutional features typical of most EMs tend to amplify and propagate shocks. Even when asset price-led cycles are not generated within EMs, they tend to be affected the most due to capital flows.

The 2008 financial crisis has emphasized the importance of macro financial linkages. In the financial sector, attention is now focusing on macro prudential regulations that are geared toward the stability of the financial system as a whole. In the macro arena, the recognition that price stability was not sufficient to guarantee macroeconomic stability and that financial imbalances developed despite low inflation and small output gaps has highlighted the need for additional tools (macro prudential policies) to complement monetary policy in countercyclical management. Emerging markets (EMs) face different conditions and have key structural features that can have a bearing on the relevance and efficacy of policy measures. Drawing on Canuto, Otaviano, and Swati R. Ghosh, eds. 2013. Dealing with the Challenges of Macro Financial Linkages in Emerging Markets. Washington, DC: World Bank), this note discusses the challenges of dealing with macro financial linkages and explores the policy toolkit available for dealing with systemic risks, particularly in the context of EMs.

Confidence in conventional financial stability regimes was shattered by the scale of the financial crisis. This book chapter explores the need for coordination between monetary policies and macro prudential…